by Andrea Carson | Sep 20, 2023 | Entrepreneurship, Finances, Taxes

As an entrepreneur, managing your business expenses is a critical component of maintaining a healthy financial foundation. Keeping a close watch on your expenses not only ensures that you stay within budget but also provides valuable insights into your business’s financial health and growth potential. In this blog, we’ll delve into effective strategies and tools to help you stay on top of your business expenses, streamline your financial processes, and set the stage for success.

1. **Create a Dedicated Business Account**

Separating your personal and business finances is essential. Open a dedicated business bank account to ensure that all your business transactions are centralized and easy to track. This separation simplifies record-keeping and prevents confusion when categorizing expenses, making it easier to prepare accurate financial statements come tax time.

2. **Digital Expense Tracking Tools**

Embrace technology by using digital expense tracking tools tailored for entrepreneurs. Apps like QuickBooks, FreshBooks, and Expensify offer user-friendly interfaces that help you record expenses, categorize them, and generate detailed reports. These tools can automate data entry, reducing the likelihood of manual errors and saving you time.

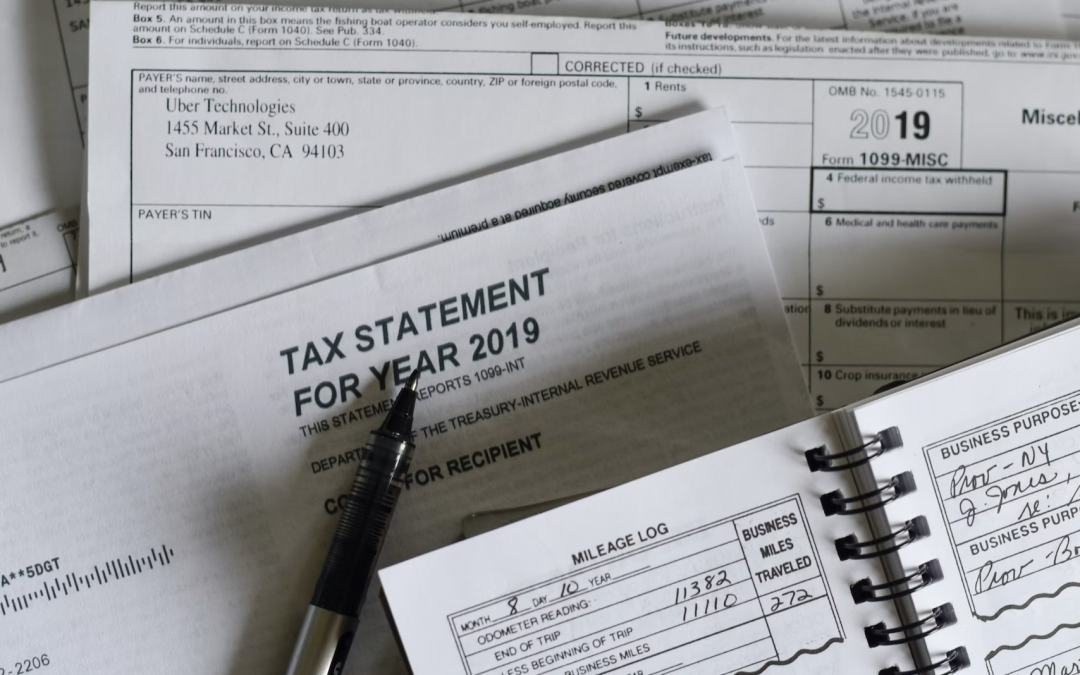

3. **Organize Receipts Digitally**

Say goodbye to the hassle of paper receipts piling up in your workspace. Utilize apps like Evernote, Shoeboxed, or Adobe Scan to capture and store digital copies of your receipts. This practice not only saves physical space but also makes it easier to search for and retrieve receipts when needed.

4. **Set Up Expense Categories**

Establish a clear and detailed system of expense categories that align with your business’s activities. Categories might include marketing, office supplies, travel, utilities, and more. Assign each expense to the appropriate category as soon as it’s incurred to streamline the tracking process and gain a comprehensive view of where your money is going.

5. **Regularly Reconcile Accounts**

Frequently reconcile your business accounts to ensure that your recorded expenses match your bank statements. This practice helps identify any discrepancies or errors early on, preventing financial confusion down the line. Reconciliation also aids in spotting potential fraudulent activities and maintaining the accuracy of your financial records.

6. **Implement a Receipt Approval Process**

If you have employees or contractors making business-related purchases, establish a receipt approval process. Require them to provide receipts and detailed explanations of their expenses before reimbursement. This not only encourages responsible spending but also adds an extra layer of accountability.

7. **Schedule Regular Expense Reviews**

Set aside time on a weekly or monthly basis to review your business expenses. Analyze spending patterns, identify areas of overspending, and make informed decisions about where to cut back or allocate more funds. Regular expense reviews also allow you to gauge the effectiveness of your budgeting strategies.

8. **Plan for Taxes**

Don’t wait until tax season to organize your expenses. Throughout the year, keep track of deductible expenses, such as office supplies, travel expenses, and professional services. This proactive approach makes tax preparation less overwhelming and maximizes your potential deductions.

Maintaining a clear record of your business expenses is a fundamental practice that contributes to the success of your entrepreneurial journey. By establishing organized processes, leveraging digital tools, and staying vigilant about tracking your spending, you’ll gain a deep understanding of your business’s financial landscape. This knowledge empowers you to make informed decisions, optimize your budget, and ultimately pave the way for sustainable growth and profitability. Remember, the effort you invest in tracking your business expenses today will pay off in the form of financial clarity and a solid foundation for the future.

by Andrea Carson | Feb 15, 2023 | SAVE MONEY

For businesses, the time value of money is a crucial financial factor. Inflation, risk concerns, prospective investment returns, and loan interest influence business decisions. In essence, you contrast the worth of the money you have right now with the relative importance of the money you will receive or spend in the future.

The following are the steps you should take if you want to save time and money at the same time:

Lead By Example

A potent instrument is a social influence. Setting an example for your company’s other employees is one of the finest methods to help it save money. If you’re careless with money, your coworkers probably won’t be either.

For many businesses, meetings are a productivity and financial drain. Harvard Business Review notes that problems arise when meetings are planned and conducted without considering how they may affect group and solitary work time, problems occur. By default, groups frequently wind up compromising either their own needs or those of others.

When meetings are appropriately conducted, projects advance and your business expand. But when done incorrectly, meetings become a pain for your company. A technique Amazon uses to make sessions short and fruitful is to reduce the number of attendees. They operate under the maxim that only a few people are present if it takes more than two pizzas to feed everyone.

Ditch conventional marketing methods

Running advertisements on TV and in print is expensive. Instead, use inexpensive marketing strategies. Innovative digital marketing techniques are also affordable and have high potential rewards. For instance, six hours a week is all it takes to do efficient social media marketing, and setting up a Facebook and Twitter account is free

Take into Account Working from Home

The advantages of remote labor are numerous. First, people are increasingly choosing remote work because it offers a better work-life balance. Also, the company has financial benefits, such as a more adaptable workforce and lower office space expenditures.

Improve the Comprehension of Your Audience.

You will only save money on all levels of your business if you know who your customers are and what they want. You’ll produce inferior goods and waste money marketing to the incorrect demographic. Instead, identify your “buyer-personas” and then incorporate them into your business plan to give them something of value.

Purchase Goods in Bulk

You usually purchase anything in bulk, which results in lower prices. Buy in bulk to save money unless you are a new business worrying about short-term cash flow. It would be best to buy anything you frequently use in size to save money for your business. Think about smaller expenditures like stationery up to larger ones like software and corporate laptops.

Shop Around for the most excellent price.

It’s frequently a good idea to haggle for a lower price. This could apply to software services, catering services, or your internet service provider.

Of course, bargaining is an art in and of itself. Think about the goods and services your company utilizes and how you might effectively haggle with suppliers to get a better deal (while retaining a good relationship with them.) If you’ve never done anything before, start gently and take advice from the experts.

Cease Paying Underperforming Workers.

A worker must be efficient in their position. If not, think about either of the following options: End their contract or put more effort into assisting them in improving their performance. Overly sentimental behavior will only benefit your company and positively impact other staff members’ morale.

Have Perks Instead of benefits

Instead of offering employee benefits, perks may be more cost-efficient and valuable. This is because, when appropriately used, bonuses can be viewed as having a higher value than comparable benefits. The utility and perceived thoughtfulness are frequently where the value lies.

Free munchies or Spotify subscriptions are two instances of this. They might only incur a tiny expense for the company, but they give employees a greater appreciation than a pay increase would.